![[Justin Donald] - Optin Preview](https://lifestyleinvestor.com/wp-content/uploads/2020/12/Justin-Donald-Optin-Preview-e1607533704966.png "[Justin Donald] - Optin Preview")

Last week, I shared the five filters I use to evaluate any deal. This week, I want to talk about an investment that doesn’t fit neatly into any of those categories, but that I believe outperforms everything else over the long run.

When people ask me, “Justin, what’s the best tangible investment you’ve ever made?” they usually expect me to say real estate. Or private equity. Or a specific deal that crushed it.

But my answer surprises them.

World-class tax strategy.

I know. It’s not sexy. It’s not exciting. But there is nothing more important to long-term wealth creation than the plan you have with taxes. And most people are leaving a fortune on the table.

The CPA Problem

Here’s something that might be uncomfortable to hear: Most CPAs are not tax strategists. They’re compliance specialists.

What’s the difference?

A compliance CPA files what needs to be filed. They make sure you don’t get in trouble with the IRS. They take the numbers you give them and put them in the right boxes.

A tax strategist proactively looks for ways to reduce your tax burden – legally – using strategies the IRS has laid out in the tax code. They’re not just filing. They’re planning.

The wealthiest people don’t just have a CPA. They have a tax strategist who advises the CPA.

Most people? They live tax strategy by default, which means no strategy at all. They just file taxes and pay whatever they’re told to pay.

Let Me Put Some Numbers to This

Let’s say you’re saving $30,000 a year through world-class tax strategy. And honestly, for a lot of people in our community, that number is light.

Over 10 years, that’s $300,000 in savings.

But here’s where it gets interesting. If you compound that at 15%, which is the average return of alternative investments over the last 40-50 years, you’re talking about over $1 million.

Over 30 years? $13 million.

That’s legacy-defining money. And most people leave it on the table because they have a CPA who files taxes instead of a strategist who minimizes them.

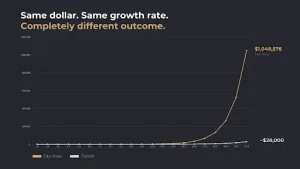

I have a chart I love to show: If you take a dollar and double it every year for 20 years – taxed vs. tax-free – the difference is staggering. The taxed version turns into about $28,000. The tax-free version? Over $1 million. Same starting point. Same growth rate. Completely different outcome.

The Litmus Test for Your CPA

Here’s a litmus test I use: If your CPA is afraid of the IRS, run.

Seriously. Get a new CPA.

Your CPA should be more confident in their skills than an IRS agent is in theirs. They should know the tax code inside and out. They should be excited to defend their work.

I was audited a while back. My CPA’s response? “Great. I can’t wait to take them on. We’re going to bury them.”

And that’s exactly what happened. Every strategy we used – all 27 of them – passed with flying colors. The IRS had to put their tail between their legs and go home.

By the way, my CPA didn’t charge me anything extra for the audit. It was part of his package. That’s how confident he is in his work.

An $800,000 Discovery

One of the members of our team, Dane, had been with the same CPA for 10 years. The guy was great… for where Dane was 10 years ago. But somewhere along the way, Dane outgrew him and didn’t even realize it.

Within his first month in our community, after sitting in on a few calls about tax strategy, Dane realized: “Oh. The biggest opportunity for me right now isn’t deal flow. It’s my taxes.”

He interviewed a few of the tax strategists we recommend. The one he chose found over $800,000 in depreciation that his previous CPA had missed over the prior couple of years.

The membership paid for itself several times over, before he ever did a single deal.

One More Distinction: Elimination vs. Deferral

Not all tax strategies are created equal.

Some strategies eliminate taxes. Some strategies defer them.

Here’s something to keep in mind: Taxes are as low as they’re probably ever going to be in our lifetime. They’re almost certainly going up from here, regardless of who’s in office.

So be careful with deferral strategies that push your tax bill into a future where rates are higher. Sometimes deferral makes sense. But tax elimination strategies – where you legally don’t owe the taxes at all – are almost always better if you can find them.

The Biggest Opportunity in a Generation

Tax strategy is one of the highest-ROI moves you can make. But there’s something else happening right now – something bigger – that I think represents the greatest wealth-building opportunity in a generation.

It has to do with a massive transfer of wealth that’s already underway. And if you position yourself correctly, the next 10-15 years could be transformational.

I’ll break it down for you next week.

Until then,

Justin

P.S. Quick question: When’s the last time your CPA brought you a proactive tax strategy – not just filed what you gave them, but actually said, “Hey, here’s something we should be doing to reduce your taxes”?

If you can’t remember, that might be telling you something. Send me an email and let me know – I’m curious how common this still is.

Keep Learning

The Private Credit Strategy That Creates Predictable Cash Flow with Andrea Propp – EP 289

The Real Reason Entrepreneurs Can’t Stay Focused with Behavioral Design Expert, Nir Eyal – EP 288